US regulators have began the compliance clock for stablecoin issuers, with a proposed customer-identification rule that may make direct minting, redemption, and account relationships look extra like financial institution onboarding.

The larger battle begins after that first buyer verify. Stablecoins will be purchased, transferred, and used throughout exchanges, wallets, DeFi venues, and good contracts lengthy after a token leaves the issuer’s direct relationship.

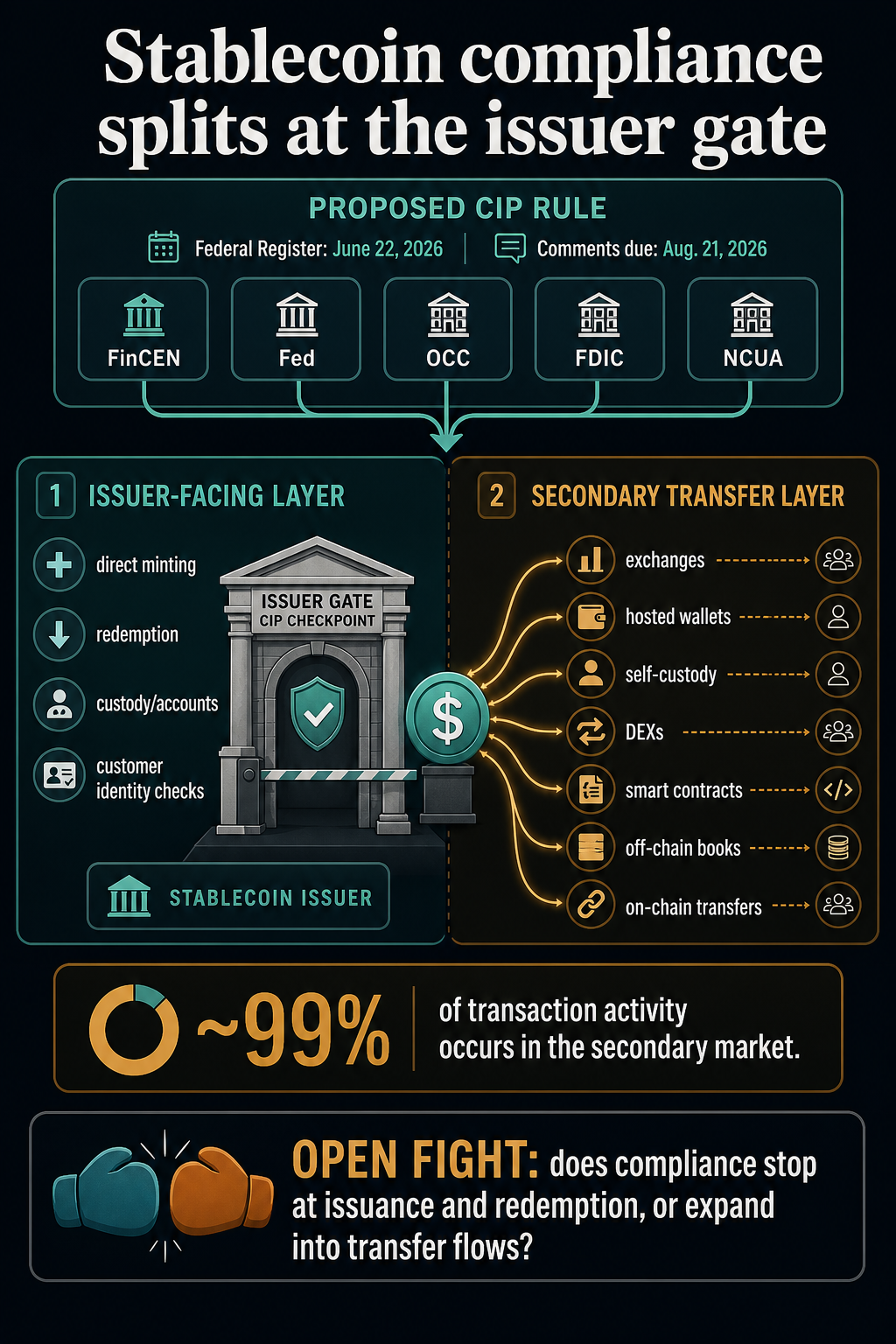

A joint proposal from FinCEN, the Federal Reserve, the OCC, the FDIC, and the NCUA would require permitted fee stablecoin issuers to run a written Buyer Identification Program, or CIP, as a part of their anti-money-laundering controls.

The Federal Register discover, printed June 22, units up a remark interval that runs via Aug. 21.

The companies are treating the rule as greater than a fringe compliance replace. Within the official discover textual content, they are saying roughly 99% of stablecoin transaction exercise happens within the secondary market and that just about all customers of fee stablecoin merchandise are secondary-market customers.

That single reality turns a technical CIP rule right into a market-structure battle.

The proposed rule would formalize identification checks the place an issuer has a direct account relationship with a buyer. As drafted, it leaves change trades, pockets transfers, DeFi swaps, and smart-contract interactions outdoors a direct issuer KYC occasion when no formal issuer relationship exists.

That leaves stablecoins going through a two-layer future: a regulated gate the place tokens are minted, redeemed, or held via issuer-facing relationships, and a switch layer the place most utilization occurs via exchanges, wallets, ledgers, and good contracts which will sit outdoors the issuer’s direct management.

Issuer relationships have gotten bank-like

The proposed rule follows the GENIUS Act’s course to deal with permitted fee stablecoin issuers as monetary establishments below the Financial institution Secrecy Act. The companies need issuers to keep up a written CIP applicable to their measurement and enterprise, with risk-based procedures to confirm buyer identification.

In sensible phrases, issuers would wish procedures designed to type an affordable perception that they know the true identification of every buyer. For people, that factors towards acquainted info reminiscent of authorized title, date of delivery, deal with, and an identification quantity.

For authorized entities, it factors towards comparable figuring out info and verification procedures.

These necessities are acquainted in banking, broker-dealer, and money-transmission contexts. They’re much less easy with stablecoins as a result of the token can proceed to flow into after the preliminary buyer relationship ends.

The proposal’s account definition does a variety of work. It focuses on a proper relationship with the issuer to acquire monetary companies or merchandise, together with minting, redeeming, custody, or different companies provided straight by the issuer.

It additionally excludes exercise by which no formal relationship is established with the issuer, together with exercise that doesn’t straight contain the issuer as a transaction occasion, aside from via a sensible contract.

That distinction turns issuer compliance right into a gatekeeping rule as an alternative of a common identification layer for each token motion. A consumer who mints straight with an issuer is in a unique place from a consumer who buys the identical stablecoin from one other dealer, an change stability, a pockets switch, or a DeFi pool.

That gatekeeping mannequin additionally explains why the proposal is greater than a guidelines for issuers. It determines the place stablecoin compliance will be confidently connected: on the level the place an organization acknowledges a buyer, data a relationship, and may preserve procedures over time.

The more durable query begins when that very same greenback token is circulating amongst folks and venues the issuer could by no means see.

The secondary market is the place the stress builds

The companies acknowledge the secondary-market downside straight. Their discover discusses the potential advantages of amassing buyer info past direct issuer relationships, but in addition says doing so can be virtually difficult as a result of issuers have restricted capability to gather info as soon as stablecoins transfer away from direct interactions.

That’s the unresolved battle on the middle of the proposal. If the compliance perimeter stops at issuance and redemption, issuers turn into extra like regulated doorways into and out of the stablecoin system.

If regulators later push identification expectations into secondary-market flows, the impact might land on exchanges, hosted wallets, DeFi entrance ends, fee processors, analytics distributors, or issuer-controlled smart-contract infrastructure.

The rule textual content retains these venues distinct. It describes secondary-market exercise as together with on-chain blockchain transactions and off-chain ledger or ebook transactions at third-party exchanges, and notes that the majority retail buying and selling happens off-chain.

That distinction is essential for readers who would possibly assume the talk is just about DeFi.

DEXs and good contracts are essentially the most seen edge case as a result of they take a look at whether or not compliance can observe token motion with out an middleman account relationship. However the bigger query additionally extends to centralized buying and selling venues, app-based wallets, fee flows, custody merchandise, and inner change ledgers, the place customers could by no means work together with the issuer.

A bank-style CIP requirement on the major layer is administratively acquainted. A secondary-market identification regime can be a unique form of undertaking, as a result of it must resolve which actors are liable for amassing info, which transfers are coated, and the way far the duty follows a token after issuance.

The most secure studying of the proposal is that regulators are beginning the place the issuer relationship is clearest. Direct minting and redemption already create a customer-facing gate. The issuer can request identification info, confirm it, preserve data and lists, and design procedures for the connection.

Permissionless switch flows work otherwise. A stablecoin could transfer via a sensible contract, a liquidity pool, a self-custody pockets, a centralized change ebook, or a fee app with out the issuer having to open a brand new account for every holder.

The proposal doesn’t, on its face, make the issuer liable for figuring out each secondary-market consumer.

The companies’ personal dialogue factors to the subsequent regulatory battleground. If nearly all transaction exercise happens within the secondary market, then primary-market CIP guidelines could make issuer doorways extra bank-like whereas nonetheless leaving open how far identification checks ought to journey into the locations the place stablecoins are literally used.

For DeFi, the query is very delicate as a result of a broader rule might stress interfaces, pockets suppliers, or protocol-adjacent companies even when the good contract itself has no typical buyer file.

For centralized venues, the query is extra more likely to concern coordination amongst regulated intermediaries, issuer reliance, knowledge sharing, and whether or not current change or money-services compliance covers the coverage hole regulators are nervous about.

The proposal due to this fact creates a compliance break up slightly than closing the talk. Issuers get a clearer path for direct clients. Secondary-market platforms and customers obtain a sign that regulators see the exercise, perceive its scale, and are asking the place to attract the road subsequent.

The remark window is the subsequent market sign

The dwell deadline provides the trade a brief runway. Feedback are due Aug. 21, 60 days after the Federal Register publication.

That creates a concrete window for issuers, exchanges, pockets firms, DeFi builders, banks, client teams, and compliance distributors to argue over the place the stablecoin identification perimeter ought to cease.

The important thing query is the place identification checks ought to finish. The proposal strongly factors towards direct buyer identification on the issuer gate.

The open subject is whether or not the ultimate rule, steerage, or future rulemaking maintains compliance there or begins constructing a bridge to secondary-market exercise.

If the ultimate rule retains the present construction, stablecoins could evolve with a extra bank-like major layer and a still-contested switch layer.

Issuers would face clearer obligations when clients come on to mint, redeem, or preserve accounts, whereas most consumer exercise would proceed to be ruled via exchanges, wallets, DeFi interfaces, and different intermediaries below their very own authorized frameworks.

If regulators transfer additional, the stablecoin market might face a extra consequential redesign. Id checks might turn into much less about who enters via the issuer and extra about which venues, interfaces, and repair suppliers should police token motion after issuance.

The proposal extends past the compliance division, as stablecoins are helpful exactly as a result of they’ll transfer throughout platforms.

Regulators at the moment are formalizing buyer checks on the issuer’s door, whereas the biggest share of exercise happens outdoors that door. The following battle is whether or not that break up stays a sensible compromise or turns into the place to begin for a broader stablecoin identification regime.